I’ve been writing about the series of self-created exemptions the Internal Revenue Service (“IRS”) has been using to evade oversight of its rulemakings. One of those exemptions is tied to White House review pursuant to Executive Order 12,866 at the Office of Information and Regulatory Affairs. Today, for the first time, the agency publicly revealed that it is in talks with the Office of Management and Budget (“OMB”) to review that exemption.

The Trump Administration’s Departments of Health and Human Services (“HHS”), Labor, and the Treasury just released a proposed rule that would allow Americans to buy short-term health insurance plans that would not be affected by the Patient Protection and Affordable Care Act’s mandates that are driving up premiums and limiting choice. Housed within that proposed rule is a microcosm of the problem I’ve been highlighting.

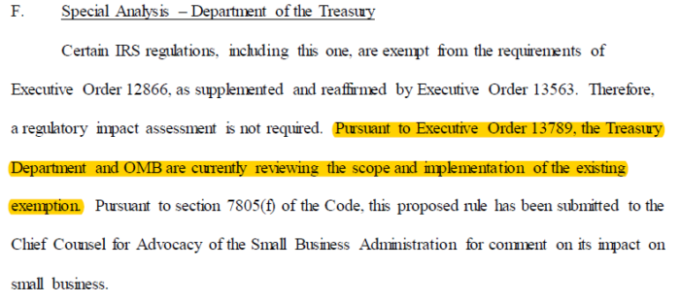

On pages 17–28, HHS and Labor conduct a series of regulatory assessments, including an explanation of what the costs, benefits, advantages, and disadvantages of the proposed rule are. They even include an analysis of the number of enrollees likely to take advantage of the proposal and the impact on the individual market exchanges. IRS? Not so much. As has been its practice, the IRS simply claims that “[c]ertain IRS regulations, including this one, are exempt from the requirements of Executive Order 12866 . . . Therefore, a regulatory impact assessment is not required.”

However, the IRS also reveals that CoA Institute’s efforts to urge the Trump Administration to review the exemption is starting to bear fruit. The IRS states that “[p]ursuant to Executive Order 13789, the Treasury Department and OMB are currently reviewing the scope and implementation of the existing exemption.”

IRS Section from Proposed Rule on Short-Term Insurance

Here’s hoping they go further than simply review the scope and implementation, and resolve to end the practice that allows the IRS to give short shrift to the impacts of its rules, while other agencies, like HHS and Labor here, do their homework.

James Valvo is Counsel and Senior Policy Advisor at Cause of Action Institute. He is the principal author of Evading Oversight. You can follow him on Twitter @JamesValvo.