Executive Summary

The Consumer Financial Protection Bureau (“CFPB” or “Bureau”) is an agency unlike most any other in the history of the United States. It possesses untold power over the American people and businesses, and the heft of this power is in a single agency director accountable to no one. As Judge Kavanaugh of the U.S. Court of Appeals for the D.C. Circuit held in a since-vacated decision, “the Director enjoys more unilateral authority than any other officer in any of the three branches of the U.S. Government, other than the President.”[1]

In the Dodd-Frank Act of 2010, Congress delegated to the CFPB the power to regulate, if necessary, mandatory-binding arbitration clauses in consumer financial contracts. This power came with an important caveat: the CFPB must first conduct a study on the effect arbitration clauses have on consumers, and any regulation promulgated by the agency must be based on that study. Yet the CFPB already had the goal in mind to regulate and ban these arbitration clauses, driven largely by internal bias and promoted by third-party interests. Instead of conducting an objective study backed by peer review, the agency sought a pre-determined result, abusing junk science and methodology to get there. In doing so, it ignored the requirements of the Information Quality Act (“IQA”) and the ensuing Office of Management and Budget (“OMB”) bulletin requiring agency peer review. This paper examines the failings of the arbitration study and offers solutions to the potential new agency head to ensure future policy is informed by sound science.

Recommendations

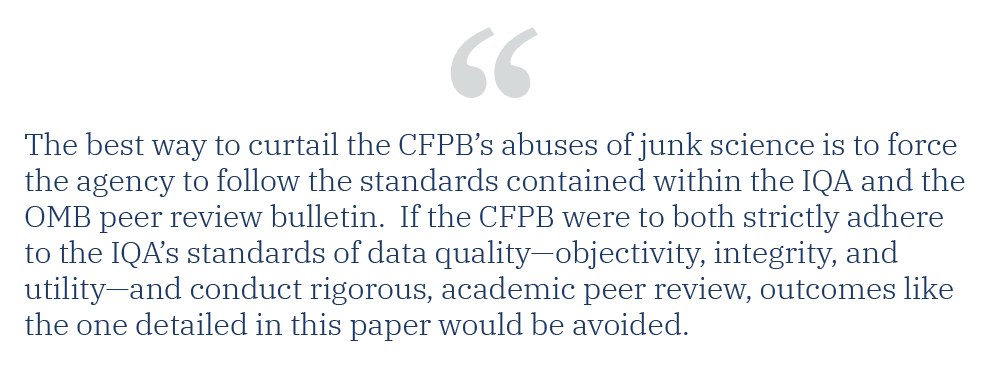

The best way to curtail the CFPB’s abuse of junk science is to force the agency to follow the standards contained within the IQA and the OMB peer review bulletin. If the CFPB were to strictly adhere to the IQA’s standards of data quality—objectivity, integrity, and utility—and conduct rigorous, academic peer review, outcomes like the one detailed in this paper would be avoided.

Cause of Action Institute (“CoA Institute”) recommends that the new CFPB Director, once confirmed, immediately institute rulemaking actions to codify these already-mandatory requirements of the IQA and peer review. This should apply to all studies or scientific findings released by the agency, whether they undergird a rule or not.[2] Although the Director could just order agency personnel to follow these directives through a memorandum, that would only be a temporary solution. Rulemaking under the Administrative Procedure Act (“APA”) would ensure that these science-based requirements have more permanence and apply regardless of who is running the agency five years from now.[3] Furthermore, the new Director should require, whether through rulemaking or otherwise, that all published scientific findings be accompanied by full disclosure of outside datasets, sources, and lobbying.

Eric Bolinder is Counsel at Cause of Action Institute

[1] PHH Corp. v. Consumer Fin. Prot. Bureau, 839 F.3d 1, 7 (D.C. Cir. 2016), vacated on reh’g en banc, 881 F.3d 75 (D.C. Cir. 2018); see Consumer Fin. Prot. Bureau v. RD Legal Funding, LLC, No. 17-890, 2018 WL 3094916, at *35 (S.D.N.Y. June 21, 2018) (“Respectfully, the Court disagrees with the holding of the en banc court and instead adopts Sections I-IV of Judge Brett Kavanaugh’s dissent[.]”).

[2] This, of course, would extend to any scientific findings that are part of a proposed rule.

[3] A future Director could institute rulemaking to reverse the requirements, but that is a cumbersome process subject to judicial review.