CoA requests access to the following records pertaining to the Internal Revenue Service’s (IRS) Exempt Organization (EO) Division for the time period January 1, 2009 to the present:

- Copies of any criteria that the IRS Cincinnati Service Center has used to assess applicants for 501(c)( 4) status;

- Communications from the Treasury Inspector General for Tax Administration (TIGTA) to the EO Division concerning any audit or investigation conducted of the EO Division;

- Copies of any Form 990 Schedule B (Schedule of Contributors) released by the IRS to a third party in response to a Freedom of Information Act (FOIA) request, as well as copies of the IRS’s FOIA response letter to that request;

- All records, including documents and emails, relating or referring to any disclosure of an exempt organization’s Form 990 Schedule B to any employee, contractor or officer of the Executive Office of the President, excluding any such records disclosed pursuant to 26 U.S.C. § 6103(c) or 26 U.S.C. § 6103(g);

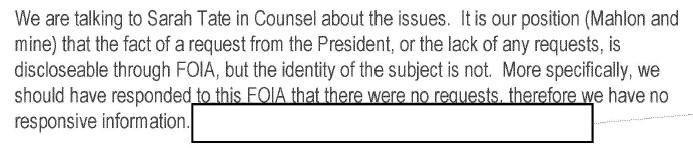

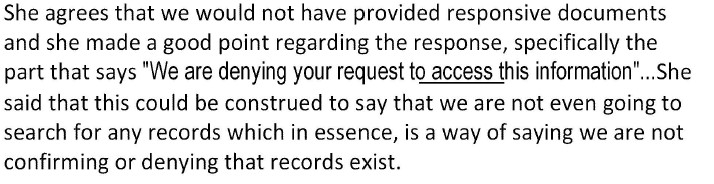

- All records, including documents and emails, referring or relating to any request from the President, Vice President, Cabinet official, employee in the Executive Office of the President, or employee in the Executive Office of the Vice President to any officer or employee of the IRS to conduct an audit or other investigation of any particular taxpayer; and a. If any requests are located in response to this item, then all communications between the IRS and TIGTA concerning those requests.

Click Here for the full request

Related work on the IRS:

FOIA Freak-Out: IRS Wrongly Denies FOIA Request, Comes Unglued Over Media Response

Cause of Action letter to the U.S. Attorney Kerry Harvey requesting an investigation of the IRS and their employees in the IRS Cincinnati Service Center in Kentucky for potential violations of the law concerning conspiracy by singling out organizations based on political views stated in their tax-exempt applications.